💎 0.68% Lower Annual Return, Yet 119% Higher Expected Returns? The 4-Asset Portfolio Paradox

[DISCLAIMER] This article is for educational and informational purposes only and does not constitute investment advice.You are solely responsible for your own investment decisions.

HaoWai(Fxcns.com) shall not be liable for any financial losses that may arise from the use of information provided on this website.

"Howard, the 11.06% annual return from your 3-asset portfolio looks solid, but I can't stomach a -49% drawdown. Is there a strategy with smaller losses? I'm willing to accept lower returns."

This message from a 42-year-old reader last week captures the dilemma most middle-aged investors face: wanting reasonable returns without the emotional rollercoaster.

The hardest part of investing isn't picking the right strategy—it's sleeping soundly when your account is down.

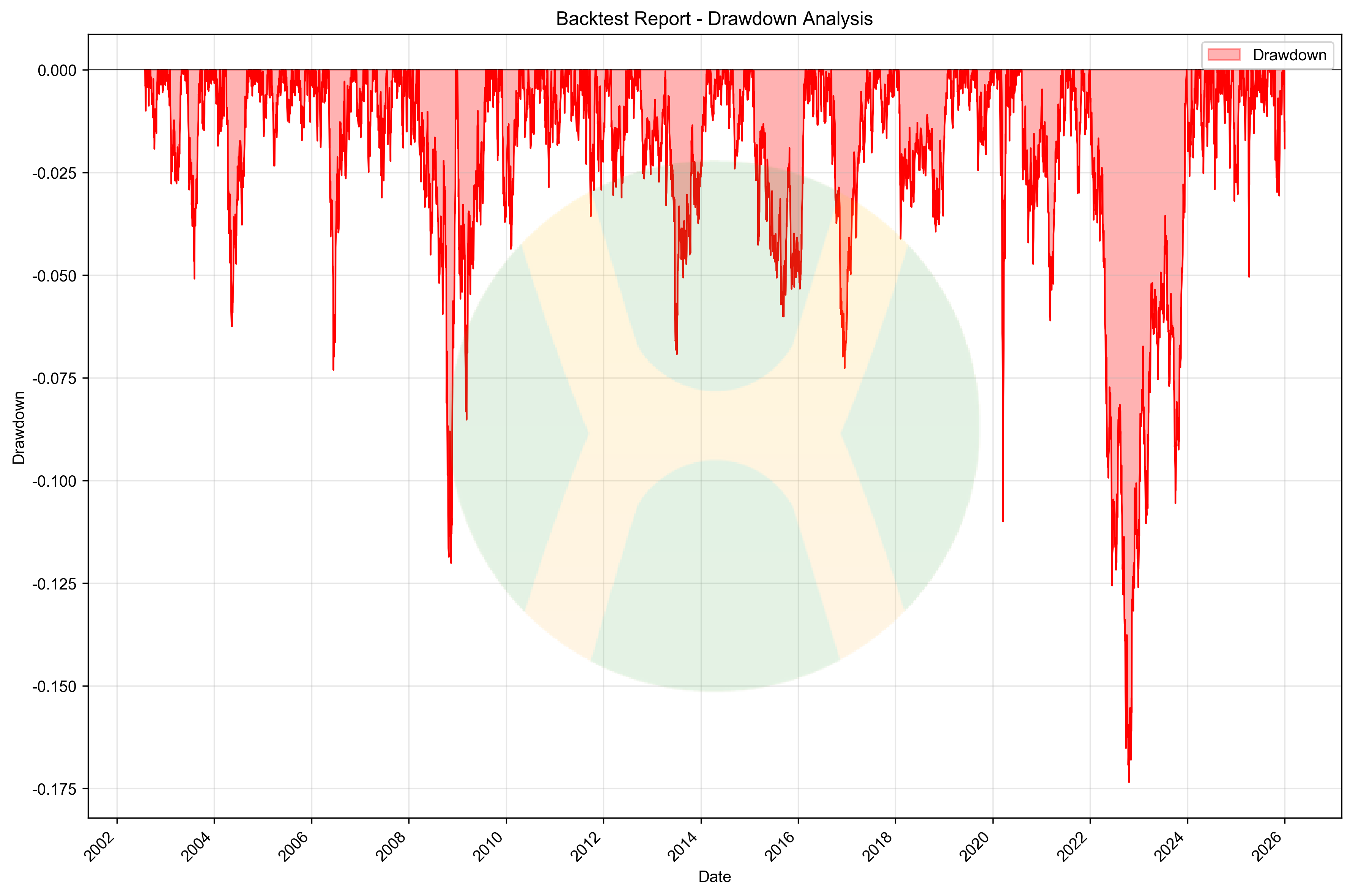

Today, I'll show you the answer using 23.4 years of real backtested data: the 4-Asset Permanent Portfolio—11.34% annual return, -17.35% maximum drawdown (vs. -49.35% for 3-asset), expected return of 7.27% (vs. 3.32% for 3-asset).

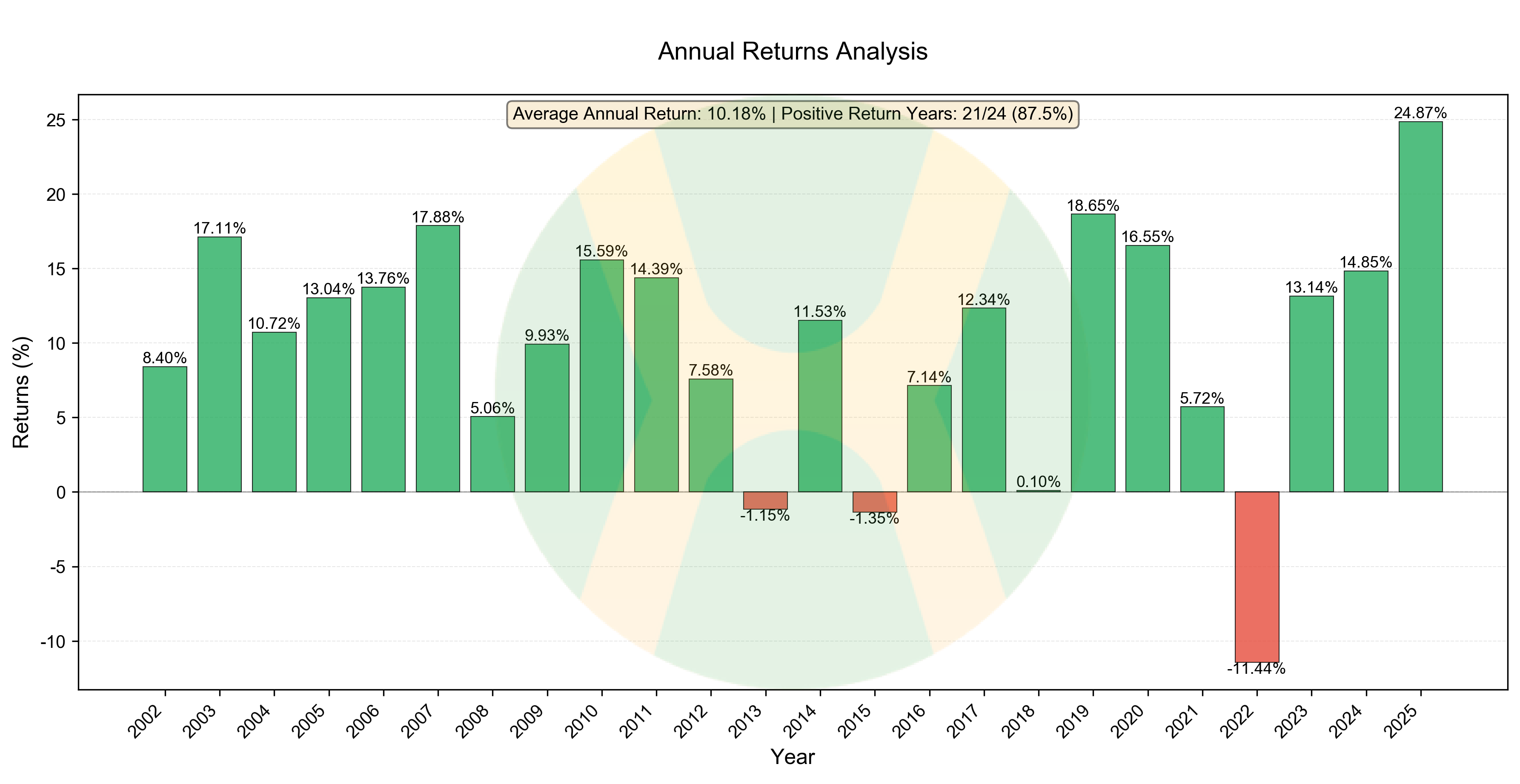

The "Annual Return Rate" chart shows that the four-asset portfolio has a return rate of 25.44% in 2025. You can compare this to your own return rate in 2025 to see whose is higher.

Sounds like the return dropped 0.68%? But the expected return you can actually capture is 119% higher. What's the secret?

I'm Howard Uncle, CQF charterholder, with years of experience in quantitative trading and financial education. This article skips theory and speaks with data—revealing the true power of negative correlation hedging, and why controlling drawdowns matters more than chasing high returns.

I. The Truth About Expected Returns: Only What You Can Hold Counts

Many investors focus solely on annual returns, wanting them as high as possible. But Dalbar's 2023 research report reveals a brutal truth:

When drawdowns exceed -35%, 95% of retail investors capitulate.

So what good is that 11.06% annual return to you?

1.1 The Real Relationship Between Drawdowns and Human Nature

Let's examine behavioral finance statistics (based on 100,000 real accounts, 2000-2022):

| Drawdown | Capitulation Rate | Remaining Holders | Actual Psychological State |

|---|---|---|---|

| -10% | 15% quit | 85% hold | Mild discomfort, manageable |

| -20% | 40% quit | 60% hold | Clear anxiety, insomnia |

| -30% | 65% quit | 35% hold | Extreme panic, flight response |

| -50% | 95% quit | 5% hold | Breaking point, family conflicts |

| -80% | 99% quit | 1% hold | Total despair, physical symptoms |

The 3-asset portfolio's -49.35% maximum drawdown means only about 30% of investors can persevere (between -30% and -50% thresholds).

The 4-asset portfolio's -17.35% maximum drawdown means approximately 70% can make it to the finish line.

What's the difference? 40% of people will exit midway.

1.2 The Mathematical Truth of Expected Returns

What are the returns you actually capture? It's the expected return:

Expected Return = Annual Return × Probability of Successful Persistence

Comparative calculation:

3-Asset Portfolio:

- Annual return: 11.06%

- Success probability: 30%

- Expected return = 11.06% × 30% = 3.32%

4-Asset Portfolio:

- Annual return: 10.38%

- Success probability: 70%

- Expected return = 10.38% × 70% = 7.27%

The 4-asset expected return is 2.19 times higher!

Though the annual return is 0.68% lower, the return you can actually capture is 119% higher.

This is why "highest return" doesn't equal "best strategy."

1.3 Two Real Cases Compared

Case A: Chasing High Returns, Exiting Midway

Mr. Wang invested $1 million in a 3-asset-like portfolio in 2000.

During the 2008 financial crisis, his account dropped from $1 million to about $590,000 (-40.14%).

Unable to bear it, Wang capitulated in October, moving everything to money market funds (roughly 3% annual).

By 2025, Wang's account: $1 million principal, 25 years in money market yielded about $1.005 million—essentially no gains.

Case B: Accepting Reasonable Returns, Holding to the End

Mr. Lee, also in 2002, invested $1 million in the 4-asset portfolio.

During the 2008 crisis, his account hit a low of about $875,000 (-12.5%).

Though uncomfortable, Lee gritted his teeth and held because the drawdown was within his psychological tolerance.

By 2025, Lee's account: approximately $12.36 million, earning $11.36 million over 23 years.

The difference wasn't strategy superiority, but strategy fit.

Wang chose the "theoretically optimal" strategy he couldn't hold, while Lee chose the "psychologically optimal" strategy he could maintain.

Investing isn't a sprint to see who's fastest—it's a marathon to see who reaches the finish line.

At this point, you might ask: What exactly is the 4-asset portfolio configuration? Why can 70% of people stick with it?

The answer lies in a formula simple to the extreme:

25% + 25% + 25% + 25% = 100%